By: Chelsey Fix

Medicare is confusing – that’s a fact! Add the confusing Medicare system on top of a complex treatment for a rare disease, and it’s easy to feel overwhelmed. The Foundation is here to help all of our patients navigate health insurance headaches! For now this article explains the current Medicare situation for our friends living with CIDP and MMN who are on Medicare and want to access home infusion for their IVIG treatments.

Let’s start with a quick review of Medicare and its parts:

- Medicare Part A

- Everyone is automatically enrolled in Part A when they apply for Medicare

- Covers hospital costs

- No monthly premium, but there is a high deductible (the amount you have to pay out of pocket before costs are covered)

- Considered part of the “Original Medicare” benefits

- Medicare Part B

- Everyone is automatically enrolled in Part B when they apply for Medicare, and most people pay a monthly premium for this coverage

- Medicare pays 80% of Medical costs

- You can purchase a Medigap plan (often called a supplemental plan) to cover the other costs, including the 20% “copay” required by Medicare. The Foundation strongly recommends that people with Medicare purchase a Medigap plan

- Note- Medigap plans are not always offered to people under 65 years old. Contact the Foundation for help with this situation.

- Covers doctors’ visits, general outpatient services, and some prescriptions, and is considered one of the “Original Medicare” benefits

- Medicare Part C

- Medicare Advantage Plans

- Provided by a private insurer that follows rules set by the Medicare office

- Most plans follow the coverage guidelines of Part A and Part B, with some prescription drug coverage benefits

- Advantage plans may be most beneficial to people under 65 years old that are on Medicare because of disability that cannot purchase a Medigap plan

- However, Advantage plans do not replace Medigap plans for those that can purchase them

- Medicare Part D

- Distributed by a private insurance company that follows rules set by the Medicare office

- Plans help to cover the cost of prescription drugs; you are responsible for either a flat copay or a percentage of each prescription

- There is no limit on out of pocket costs under Part D, but the plan is designed to help lower costs for prescriptions where possible through something called “catastrophic coverage” (more on that in the table below)

- There is no Medigap plan available to help with out of pocket costs, such as copays

Now the important part – what does it mean if you have CIDP or MMN and want to infuse at home? Currently, there is no benefit under Medicare that specifically covers home infusion. That means that some home infusion providers will work with you if you bought a Medicare Part D plan to provide the service, but they are not obligated to do so. The Foundation wants everybody to have the choice of where they get their IVIG infusion, regardless of their insurance. That is why we have worked with Congress to introduce HR 2905 – the Medicare IVIG Access Enhancement Act. HR 2905 will create a law for a “demonstration project”, which is a fancy way of saying that Medicare will let people with Medicare Part B decide to get home infusion if they want to. Meanwhile, the Medicare team will monitor the cost and health of patients, and after 3 years will decide if Medicare should cover home infusion for CIDP and MMN patients forever. It is important to remember that this is always voluntary for patients – HR 2905 does not force anybody to choose home infusion!

Because Medicare is so confusing, it is natural to be worried about what it would cost to get home infusion through that system. Here’s the breakdown of your potential costs in Medicare Part B or Medicare part D:

| Medicare Part B (what would happen if HR 2905 becomes law) | Medicare Part D (only some home infusion providers accept Medicare Part D) | |

| Monthly Premium | Fixed rate: $144.60/month | Cost varies, Average $42.05/month |

| Other costs | Purchase a Medigap plan – $150/month Medicare Deductible: $198/year | Deductible: $435/year Initial Coverage Phase: $1,005/year Coverage Gap Out of Pocket: $1,588/year Catastrophic Coverage Out of Pocket: $9,000/year (estimate) |

| What is covered by Medicare? | Typical Medicare services & visits, PLUS -IVIG drug -cost of nursing for home infusion -cost of equipment for home infusion | Typical Medicare services, PLUS -IVIG drug |

| Estimated cost paid by patient per year | Approximately $4,000 | Approximately $13,000 |

| Important points to remember | -The cost of a Medigap plan is different for everyone based on where live, your age, and the type of plan you purchase -Many Medigap plans cover the 20% copay typically required by Medicare Part B AND set out of pocket spending limits -This accounts ONLY for the cost of home infusion; your yearly medical expenses may also add to what you spend out of pocket | -When a person is using the “Catastrophic Coverage” feature of Medicare, they will pay 5% of the total cost of each medication until the end of the calendar year. You may pay more or less than our estimate here depending on your IVIG brand, frequency of treatment, etc. There is no out of pocket spending limit. -Some specialty pharmacies offer financial assistance programs to some people, which can help to lower your out of pocket cost; your specialty pharmacy cannot advertise this program so make sure you ASK if they can offer help -There may be other financial assistance programs through Medicare or your state government. The Foundation is happy to help you learn more about one of those programs -This accounts ONLY for the cost of home infusion; your yearly medical expenses may also add to what you spend out of pocket |

.

As you can see, our goal is to make home infusion accessible in Medicare Part B because it will be more affordable. It is important to note that the cost is lower because Medigap plans cover the cost of everything that Medicare does not cover, and those plans are only available if you are using Medicare Part B. Also, Medicare allows for yearly changes to your coverage, so be sure to track your expenses closely and make changes during the yearly “Open Enrollment” period to find a plan that helps to meet your needs.

Although some specialty pharmacies (or home infusion providers) have financial assistance programs, eligibility for financial assistance is determined by the companies on a yearly basis. HR 2905 would create a benefit for home infusion so that patients would not need to rely on financial programs. Because not everyone is eligible for these programs, HR 2905 creates a more equal path to getting home infusion of IVIG. And, since some specialty pharmacies do not accept Part D plans, HR 2905 would make sure that specialty pharmacies cannot turn away patients because of their Medicare coverage. Instead, HR 2905 gives the power to create a treatment plan and location solely to you and your doctor.

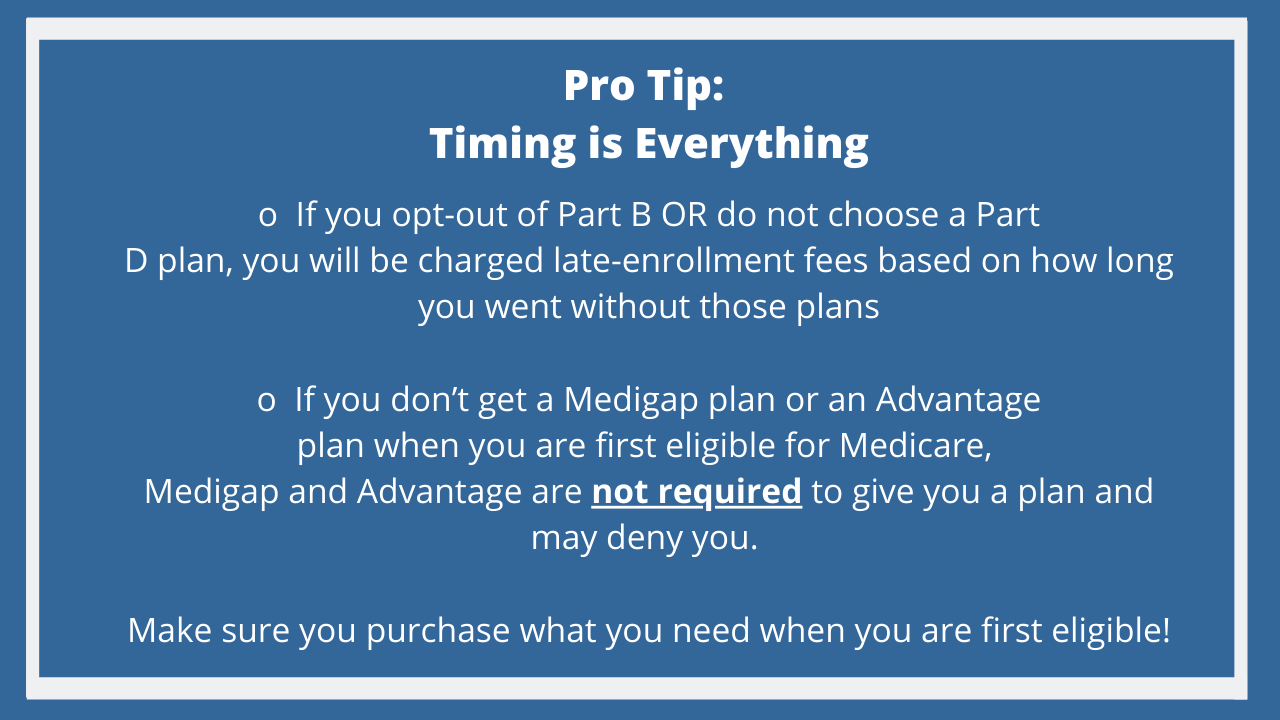

There is a slight chance that some patients are not able to buy a Medigap plan because of their age (under 65) and state in which they live. If you run into this problem at any point, please contact the Foundation for help troubleshooting your situation.

Finally, it is also important to remember that HR 2905 creates a law for a demonstration project, meaning that for the first 3 years the Medicare Part B coverage is not permanent. These first 3 years are considered a “trial period”, and Medicare will measure the cost of having home infusion in Part B. While the demonstration project is going on, people with Medicare Part D plans who have an arrangement with a specialty pharmacy will still be able to use their Part D plan for home infusion. When the demonstration project is over, Medicare may decide to make the Part B benefit permanent (that’s our hope!). It is also important to know that HR 2905 was modeled after an existing project in Medicare that is exclusive to patients living with Primary Immune Deficiency (PID). The PID project is coming to a close, and Medicare is currently reviewing the data that was collected from that project to make a decision on IVIG at home for PID patients using Medicare.

We hope this helps you to make decisions about your Medicare coverage and site of infusion care. The Foundation is available to answer any of your questions! In the meantime, we hope that you will visit our Advocacy Action Center to help us make HR 2905 and the demonstration project happen. CLICK HERE to tell your Congressperson to support the bill that will take the first steps towards getting home infusion covered by Medicare Part B!

Contact:

Chelsey.Fix@GBS-CIDP.org with questions!

Other Financial Resources:

See if you qualify for a low-income subsidy – https://www.ssa.gov/benefits/medicare/prescriptionhelp/

See if your state offers extra help: https://www.medicare.gov/pharmaceutical-assistance-program/state-programs.aspx

Learn about when to enroll in each program:

https://www.medicare.gov/your-medicare-costs/part-b-costs/part-b-late-enrollment-penalty

https://www.medicare.gov/drug-coverage-part-d/costs-for-medicare-drug-coverage/part-d-late-enrollment-penalty

https://www.medicare.gov/supplements-other-insurance/when-can-i-buy-medigap

Other Articles You May Like

Claire, Recipient of the Benson Research Fellowship: One Step Closer to a Cure

For Dr. Claire Bergstrom Johnson, becoming a scientist wasn't just a career choice—it was personal. When her…

Julie Bell’s Clinical Trial Journey: Why She’d Participate Again

In rare disease communities like ours, progress in drug development is often slow, in part…

GBS|CIDP Foundation Partners with UNITAR to Advance Global Plasma Access

The Foundation is proud to officially partner with United Nations Institute for Training and Research…